When state legislatures in the United States implemented the first sales tax laws to boost revenues in the 1930s, the American economy depended on the manufacture and sale of physical goods. Typically, early sales tax laws allowed only the taxation of “tangible personal property” (TPP), rather than taxing services.

As the United States has shifted from a manufacturing-based economy to a service-based economy, many states started to impose sales and use tax on services as well. Many businesses that provide services are still unaware of these statutory changes—some mistakenly believe they don’t have to pay any sales tax at all, even if they’re selling services all over the United States.

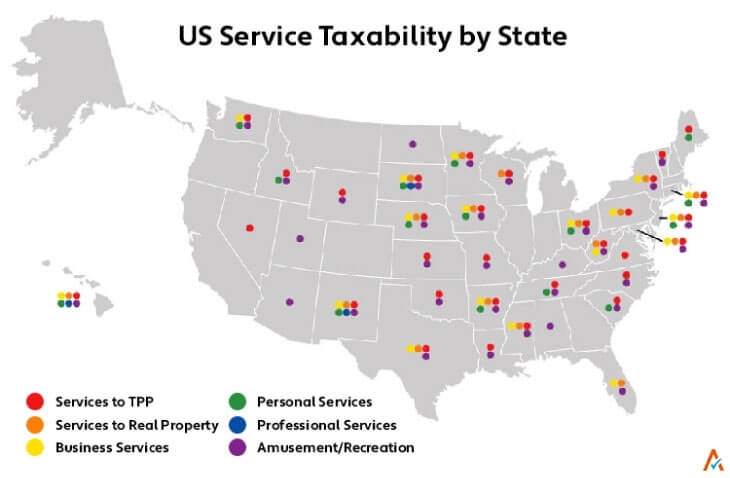

This guide is designed to provide an overview of the complexity of sales tax on services by state.

Five U.S. states (New Hampshire, Oregon, Montana, Alaska, and Delaware) do not impose any general, statewide sales tax, whether on goods or services. Of the 45 states remaining, four (Hawaii, South Dakota, New Mexico, and West Virginia) tax services by default, with exceptions only for services specifically exempted in the law.

This leaves 41 states — and the District of Columbia — where services are not taxed by default, but services enumerated by the state may be taxed. Every one of these states taxes a different set of services, making it difficult for service businesses to understand which states’ laws require them to file a return, aswell as which specific elements of their services are taxable.

No two states tax exactly the same specific services, but the general types of services being taxed can be divided roughly into six categories.

Services to TPP: Many states have started to tax services to tangible personal property at the same rate as sales of TPP. These services typically improve or repair property. Services to TPP could include anything from carpentry services to car repair.

Services to real property: Improvements to buildings and land fall into this category. One of the most commonly taxed services in this area is landscaping and lawn service. Janitorial services also fall into this category.

Business services: Services performed for companies and businesses fall into this category. Examples include telephone answering services, credit reporting agencies and credit bureaus, and extermination services.

Personal services: Personal services include a range of businesses that provide personal grooming or other types of “self-improvement.” For example, tanning salons, massages not performed by a licensed massage therapist, and animal grooming services can be considered “personal services.”

Professional services: The least taxed service area, in large part because professional groups have powerful lobbying presences. Professional services include attorneys, physicians, accountants, and other licensed professionals.

Amusement/Recreation: Admission to recreational events and amusement parks, as well as other types of entertainment. Some states that tax very few other services, like Utah, still tax admission charges to most sporting and entertainment events.

Remember that within each category of services, states can still have drastically different regulations. For instance, both Florida and Iowa are marked as taxing “business services,” even though Iowa taxes a wide range of these services and Florida only taxes security and detective services.

For more details about the specific tax liability of your business in individual states, consult state Departments of Revenue for additional information.

| State | Business services impacted by taxation |

| Alabama | Amusement/Recreation |

| Alaska | None |

| Arizona | Amusement/Recreation |

| Arkansas | Services to TPP, Services to Real Property, Business Services, Personal Services and Amusement/Recreation |

| California | None |

| Colorado | None |

| Connecticut | Services to TPP, Services to Real Property, Business Services, Personal Services and Amusement/Recreation |

| Delaware | None |

| Florida | Services to Real Property, Business Services, Personal Services, Professional Services and Amusement/Recreation |

| Georgia | None |

| Hawaii | Services to TPP, Services to Real Property, Business Services, Personal Services, Professional Services and Amusement/Recreation |

| Idaho | Services to TPP, Personal Services and Amusement/Recreation |

| Illinois | None |

| Indiana | None |

| Iowa | Services to TPP, Services to Real Property, Business Services, Personal Services and Amusement/Recreation |

| Kansas | Services to TPP and Amusement/Recreation |

| Kentucky | Amusement/Recreation |

| Louisiana | Services to TPP and Amusement/Recreation |

| Maine | Services to TPP and Personal Services |

| Maryland | Services to TPP, Services to Real Property, Business Services and Amusement/Recreation |

| Massachusetts | None |

| Michigan | None |

| Minnesota | Services to TPP, Services to Real Property, Business Services, Personal Services and Amusement/Recreation |

| Mississippi | Services to TPP, Services to Real Property, Business Services and Amusement/Recreation |

| Missouri | Services to TPP and Amusement/Recreation |

| Montana | None |

| Nebraska | Services to TPP, Services to Real Property, Business Services, Personal Services and Amusement/Recreation |

| Nevada | Services to TPP |

| New Hampshire | None |

| New Jersey | Services to TPP, Services to Real Property, Business Services, Personal Services and Amusement/Recreation |

| New Mexico | Services to TPP, Services to Real Property, Business Services, Personal Services Professional Services and Amusement/Recreation |

| New York | Services to TPP, Services to Real Property, Business Services and Amusement/Recreation |

| North Carolina | Services to TPP and Amusement/Recreation |

| North Dakota | Amusement/Recreation |

| Ohio | Services to TPP, Services to Real Property, Business Services, Personal Services and Amusement/Recreation |

| Oklahoma | Services to TPP and Amusement/Recreation |

| Oregon | None |

| Pennsylvania | Services to TPP, Services to Real Property and Business Services |

| Rhode Island | None |

| South Carolina | Services to TPP, Personal Service and Amusement/Recreation |

| South Dakota | Services to TPP, Services to Real Property, Business Services, Personal Services Professional Services and Amusement/Recreation |

| Tennessee | Services to TPP, Personal Service and Amusement/Recreation |

| Texas | Services to TPP, Services to Real Property, Business Services and Amusement/Recreation |

| Utah | Amusement/Recreation |

| Vermont | Services to TPP and Amusement/Recreation |

| Virginia | Services to TPP |

| Washington | Services to TPP, Business Services, Personal Services and Amusement/Recreation |

| West Virginia | Services to TPP, Services to Real Property, Business Services and Amusement/Recreation |

| Wisconsin | Services to TPP, Services to Real Property and Amusement/Recreation |

| Wyoming | Services to TPP and Amusement/Recreation |

Many companies assume services delivered in conjunction with goods sold (e.g., swimming pool and pool cleaning, computers and maintenance, construction materials and installation) aren’t taxable, but that's often not the case. Delaware, Hawaii, New Mexico, and South Dakota tax most services. Still others, like Texas and Minnesota, are actively expanding service taxability.

Businesses that sell services across multiple states need to know where those services are subject to sales tax. The fact that sales tax laws often change makes it challenging to remain in compliance.

States regularly change product and service taxability rules, and the onus of staying on top of changes is on businesses. For example, Washington state lawmakers decided to tax martial arts and mixed martial arts classes in the fall of 2015. Two years later, many of those services were once more exempt. Failure to correctly apply sales tax rates and rules to products and services can lead to costly errors.

Knowing which rate to charge and which sales tax rules apply is especially challenging for companies that sell goods or services in multiple states. No two states have the same sales tax laws.

Most states now require certain out-of-state sellers to register with the tax authority then collect and remit sales tax. What's challenging is figuring out which states require which businesses to do so. That depends on nexus — the connection between a business and a state that triggers a sales tax collection obligation.

Having a physical presence in a state always triggers nexus, but thanks to the United States Supreme Court decision in South Dakota v. Wayfair, Inc. (June 21, 2018), nexus can also be created by economic activity alone (economic nexus). As of June 2020, 43 states and the District of Columbia require out-of-state businesses with a certain volume of sales or number of transactions in the state to collect and remit sales tax.

Determining nexus is the first step toward sales tax compliance.

Many businesses that provide customer support, installation, or warranty services in conjunction with the sale of a physical good need to hire an army of accountants to determine what's taxable and what's exempt. If you sell service contracts separately or in tandem with sales of tangible goods, you may be liable to collect sales tax.

While Hawaii, New Mexico, and South Dakota generally tax all sales of services, many other states tax some services but not others. The challenge for businesses is determining which services are taxable in states where they have nexus (an obligation to collect sales tax). In some states, businesses must charge sales tax on services provided in conjunction with sales of physical goods.

When a sale includes both a product and a service, some states use a true object test to determine the taxability of the transaction. If the main purpose of the transaction (the true object) is the sale of taxable property or equipment, the entire transaction is subject to sales tax. If the main purpose of the transaction is instead the sale of an exempt service, the entire transaction is generally exempt.

Combined sales of products and services are more common in some industries than others, notably the construction, manufacturing, and medical industries. For example, an insulin monitor often accompanies the sale of diabetes treatment. In this case, the product is secondary to the service, and taxability is based on the real object of the transaction — the service provided.